Posted on 04 Nov 2024

After falling steadily last month, Chinese steel prices are expected to stay rangebound within a narrow band in November, as the market is anticipating further economic incentive policies from the country's central government, according to Wang Jianhua, chief analyst at Mysteel. A possible surplus of steel supply will drag on prices if it eventuates, he also warned.

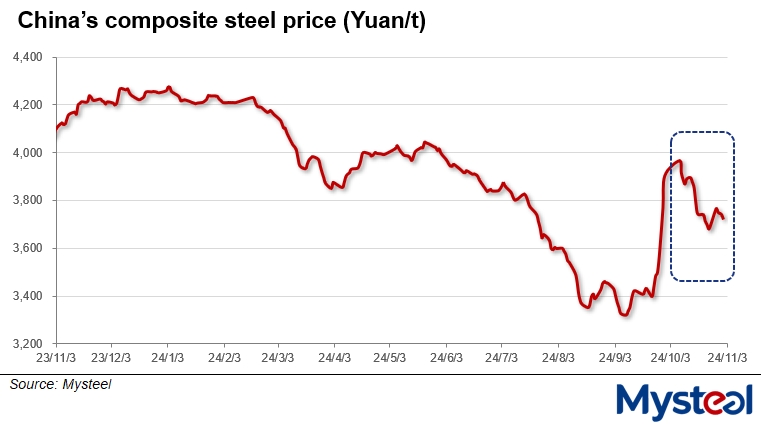

Steel prices in China briefly hovered at a seven-month high in early October before retreating rapidly amid cooled market sentiment, with the national composite steel price sitting at Yuan 3,631/tonne ($509.7/t) including the 13% VAT as of October 31, lower by a significant Yuan 313/t or 7.9% from the end of September, Mysteel's assessment shows.

"The price pullback is inevitable following the surge driven by the emotional shifts among market participants," Wang commented. "Only when the effects of the stimulus policies become evident or further supportive policies are announced can the prices be pushed up again," he added.

"The price pullback is inevitable following the surge driven by the emotional shifts among market participants," Wang commented. "Only when the effects of the stimulus policies become evident or further supportive policies are announced can the prices be pushed up again," he added.

"The NPC Standing Committee session to be held in Beijing (over November 4-8) will be a key focus for the market," Wang said, noting that so long as the policies introduced at the session meet market expectations, steel prices will regain upward momentum.

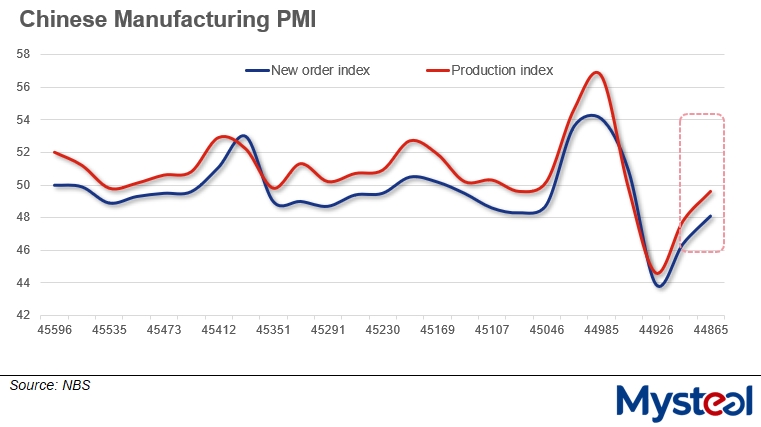

China's economic indicators such as national retail consumption, fixed asset investment, and the Purchasing Managers' Index (PMI) generally showed positive on-month growth in October, though the increments were mild, as reported. This will also lend some support for steel prices, according to Wang.

Specifically, the country's PMI for the manufacturing industry rebounded for the second month in October and returned to the expansion zone at 50.1, with the indices for production and new orders performing well, according to data released by the National Bureau of Statistics on October 31.

"Judging from the PMI, steel demand from the manufacturing sector will increase in November," Wang remarked.

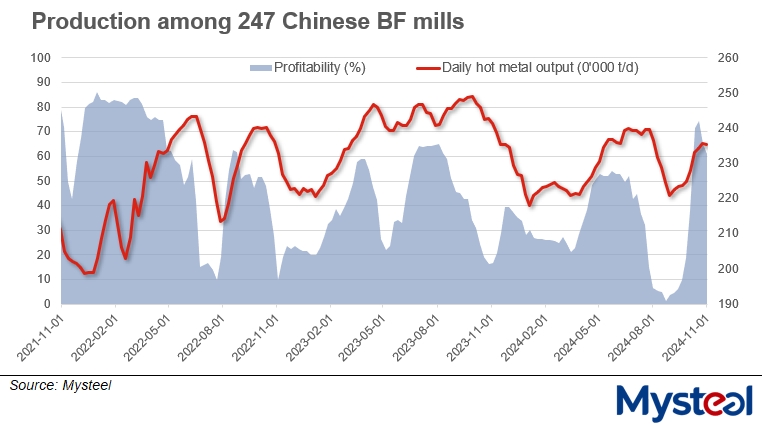

On fundamentals, however, the high production rates of steel mills will exert major downward pressure on steel prices, Wang warns.

Mysteel's survey showed that by the end of last month, the daily production of hot metal among the 247 sampled blast furnace (BF) steelmakers nationwide had risen to 2.35 million tonnes/day, getting close to the highest level for this year.

"Considering that most steelmakers can still earn some profits on selling their products, it is unlikely that the mills would be willing to scale back production soon," Wang pointed out.

"Considering that most steelmakers can still earn some profits on selling their products, it is unlikely that the mills would be willing to scale back production soon," Wang pointed out.

China's steel market may see a maximum increase of 1 million tonnes in the steel supply this month, while the growth in steel demand can hardly be expected to reach this level, he observed. As such, steel inventories may stop falling and start to accumulate across the country in November, he added.

By the end of October, the total stocks of major carbon steel products held by steelmakers and traders in the 35 Chinese cities Mysteel monitors had dropped by 1 million tonnes or 7.8% on month to 12.3 million tonnes, touching the lowest level since late December 2019.

The mills' zeal for production can easily translate to excessive supply and trigger pessimism in the market, according to Wang, but the low inventories will prevent steel prices from falling significantly, he believed.

Chinese steel prices have the potential to both gain and decline in November, but the fluctuations in market sentiment and fundamentals will likely keep the price movements limited, Wang concluded.

Source:Mysteel Global