Posted on 15 Oct 2024

|

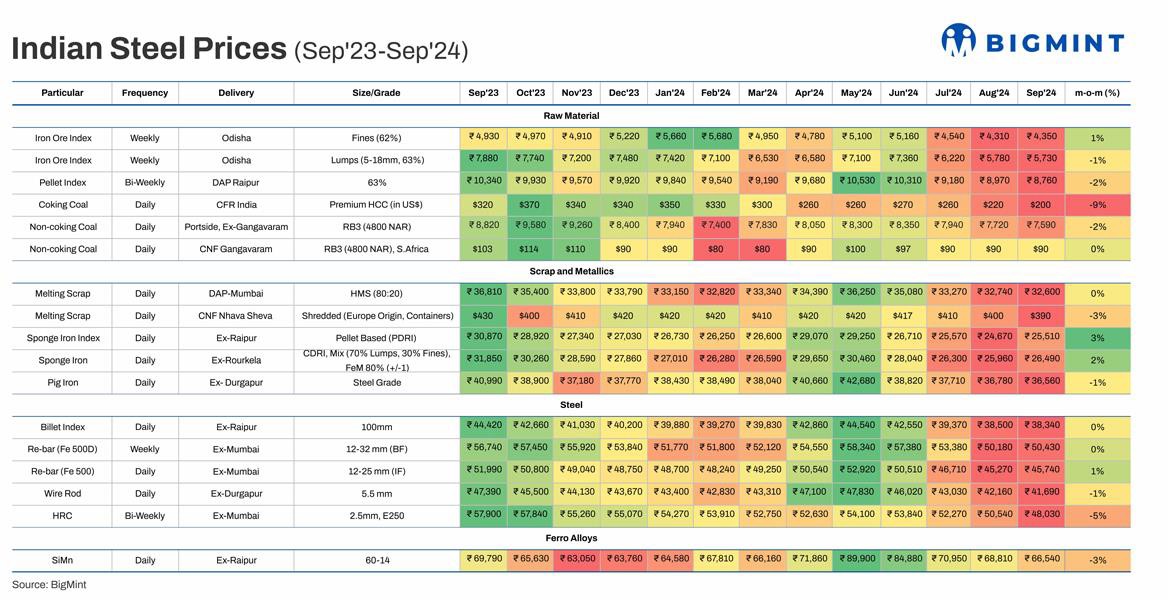

Morning Brief: India's steel and raw material prices threw up a mixed trend, though overall, the slide, seen previously, assuaged marginally in September 2024. Eight of the 17 commodities tracked dipped slightly, while the remaining upped slightly or remained flat m-o-m. Except for coking coal, which dived 9%, the rest moved in a narrow range. BigMint goes behind the scene:

Australian premium HCC coal: Average Australian premium HCC coking coal prices eroded by 9% m-o-m to $200/tonne (t) CFR India in September, 2024 from $220/t in August. Coking coal prices reduced amid weak sentiments in steel and the sustained downturn in international coke markets, coupled with increased shipments from Australia. Moreover, a fall in futures, along with demand concerns in major buying countries, weighed on offers. Domestic met coke prices fell by INR 1,000-2,000/t m-o- m in September, keeping bids lower for merchant cokeries. Indian primary mills largely book coking coal on the basis of long-term contracts. However, not much restocking was seen which kept bids on the lower side.

Indexed port-side ex-Gangavaram prices of RB3 (4800 NAR) from South Africa dropped 2% to INR 7,590/t in September 2024 from INR 7,720/t in August 2024. The decline was primarily due to weak domestic demand, increased inventory levels, monsoon-related disruptions, and competitive pressure from international suppliers. Meanwhile, CNF Gangavaram's price of the same grade remained flat m-o-m at $90/t in September 2024. Prices moved in a narrow range amid tight availability due to monsoon-related issues in domestic supplies from Coal India, and rise in sponge iron prices.

Silico manganese 60:14: Prices of the daily 60:14 grade silico manganese index in Raipur fell by 3% to INR 66,540/t in September 2024 (INR 68,810/t in August). In September, MOIL lowered prices of manganese ore. Grades above 44% saw a 20% reduction, while those below 44%, including SMGR and fines, experienced a 15% decrease. Imported manganese ore prices (of South African origin) fell from $4.15/dmtu in August to $3.93/dmtu in September. Weak manganese alloys export demand and global price drops weighed on silico manganese.

These showed a mixed trend.

Pellet-based PDRI: Pellet-based P-DRI, ex-Raipur, rose by 3% m-o-m to INR 25,510/t in September, compared to INR 24,670/t in August. In CDRI, ex-Rourkela prices also rose 2% m-o-m in September to INR 26,490/t (INR 25,960/t in August). By end- September, domestic sponge iron sentiments showed an improvement, driven by a recovery in demand and increased buying activity amid favourable prices. The slight uptick in finished steel demand also supported sponge. Export sentiments for sponge iron were relatively moderate, but the positive domestic demand outlook provided some stability for producers.

Steel grade pig iron: Pig iron prices in September 2024 slipped 1% m-o-m to INR 36,560/t (INR 36,780/t in August).

However, pig iron auction prices from both SAIL and NMDC rose by INR 1,000 -1,500/t over last month. This increase was driven by a short supply in scrap and higher demand for finished products toward month-end, leading to a rise in domestic pig iron prices across regions.

Domestic melting scrap (HMS 80:20 ex-Mumbai): These remained flat m-o-m at INR 32,600/t in September 2024 as compared to INR 33,270/t in August. Throughout September 2024, domestic ferrous scrap prices dropped by INR 100-1,000/t. The first half of the month was marked by a steady decline in both offers for and trade volumes in steel. However, by the second half, the market experienced a rebound in scrap prices, spurred by strong demand for finished steel and a tightness in scrap supply at local mills.

Imported containerised melting scrap: Prices of imported shredded scrap in containers from Europe, however, slipped 3% in September to $390/t CNF Nhava Sheva ($400/t in August). India's imports of scrap have been falling amid higher freights, and greater price viability in the domestic material. The latter worked out cheaper against INR 32,744/t seen for imported in rupee parity.

Iron ore fines and pellet prices moved in a highly narrow range in September.

Fines & lumps: Fe62% fines prices from Odisha rose a marginal 1% in September 2024 to INR 4,350/t (INR 4,310/t in August) while the Fe63% lumps (Odisha) slipped 1% m-o-m to INR 5,730/t (INR 5,780/t). Prices remained under pressure in the first half of September but bids went up post-OMC's auction. Bids rose by INR 275/t and INR 50/t for fines and lumps respectively m-o-m. The marginal increases were supported by the rise in prices of sponge iron, a competing raw material. The sponge iron index rose 3% m-o-m. Moreover, India's iron ore output dropped to a year's low to 19 million tonnes in August amid prolonged monsoons.

Pellets: The bi-weekly pellets index DAP Raipur (grade 63%), however, dropped marginally by 2% to INR 8,760/t in September (INR 8,970/t). A fall in pellet exports resulted in diversions of excess supplies from eastern India to central regions which kept prices under pressure. India's iron ore and pellet exports fell to 2 mnt in September (provisionally) against 2.1 mnt in August. Indian pellet export prices fell from $92/t FOB India in August to $87/t in September.

This segment, comprising billets and finished products, saw prices fall as demand remained slack across-the-board.

Billets: The ex-Raipur billet index remained stable m-o-m at INR 38,340/t in September 2024 (INR 38,400/t in August).

Rebar & wire rods: The ex-Mumbai BF-grade rebar was also flat m-o-m at INR 50,430/t (INR 50,180/t in August) in the period under review. On the other hand, the IF grade upped 1% to INR 45,740/t (INR 45,270/t) while wire rods (ex-Durgapur) dipped 1% to INR 41,690/t (INR 42,160/t) last month.

Rebars were better placed last month because of a shortage in supply. A longs PSU player has been operating on only one of its three blast furnaces which led to curtailment in BF-grade production. In the IF segment, some production curtailment earlier in the month rationalised inventories and supported prices. That apart, sponge and iron ore prices rose m-o-m while domestic scrap remained firm. Thus, the raw material price support also helped longs.

HRC: Ex-Mumbai trade-level HRC prices lost 5% m-o-m to INR 48,030/t (INR 50,540/t). Mills were compelled to reduce prices or keep them unchanged through last month because of the growing preference for cheaper imports from Vietnam and China. In addition, weak domestic and export demand played spoilsport.

Prices of longs steel may have bottomed out and can either remain stable or rise from here since the peak demand season is seen setting in from October. Some major mills have already effected a hike of INR 1,000-2,000/t in rebars for October sales. Flats may see some silver lining in the form of festive season demand for cars and other consumer goods. The market buzz is that tier-1 mills are also mulling a price hike in flats of INR 500-1,000/t in October.

This scenario may keep raw material prices supported.

Source:BigMint