Posted on 15 Oct 2024

*Power demand up 5%, coal-based generation rises 8% y-o-y in Jan-Aug'24

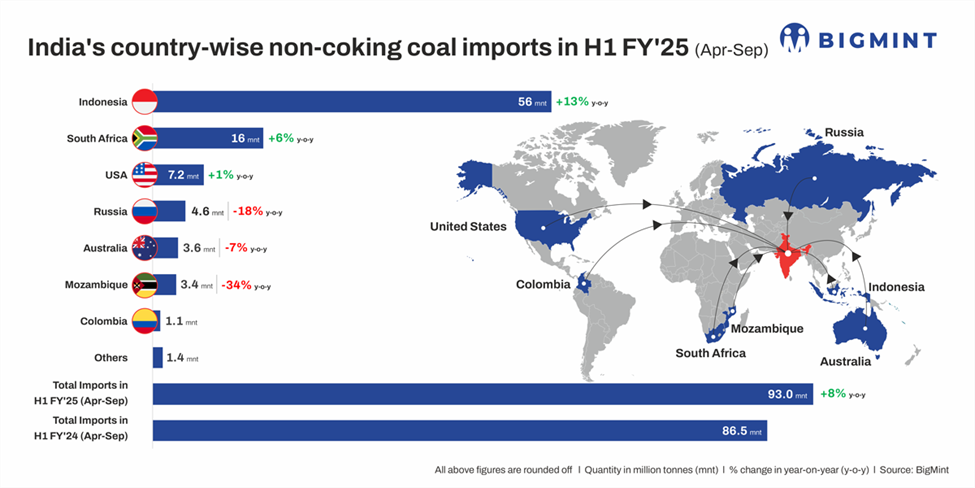

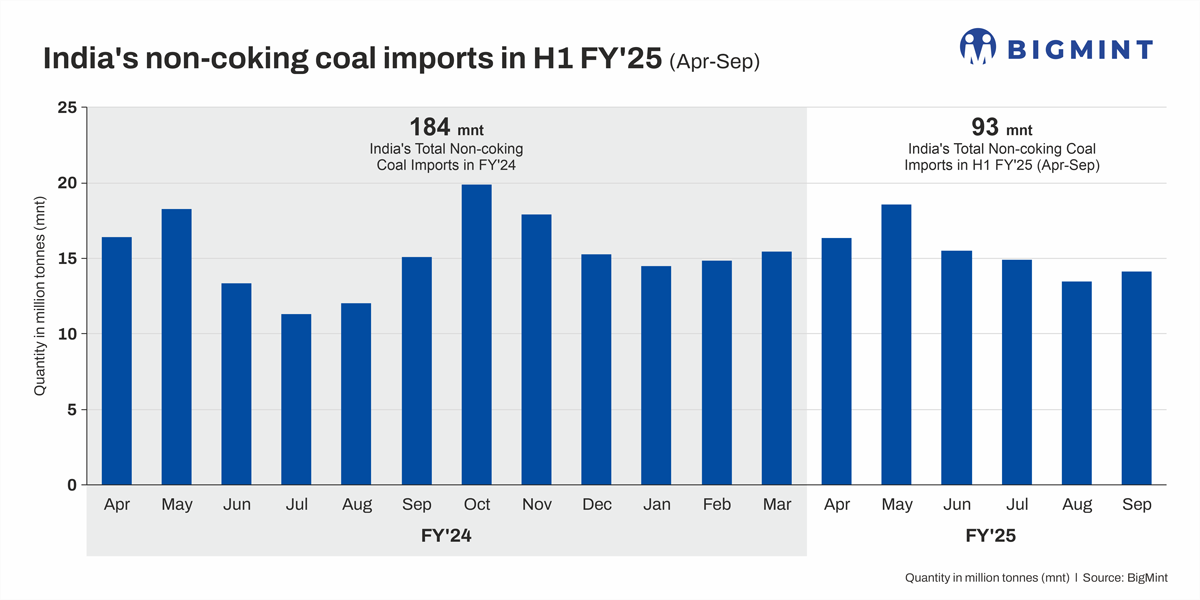

This reflects an increase of 8% y-o-y in imports of non-coking coal, which exposes India's high dependence on coal imports despite efforts aimed at import substitution spearheaded by the government.

Top exporters, buyers

The key coal exporting countries to India remained largely the same: Indonesia shipped the largest volumes during the period under review. Data shows that Indonesia exported more than 56 mnt

compared with around 50 mnt in H1FY'24, while South Africa shipped around 15.6 mnt as against 14.7 mnt in the year-ago period.

The other major coal exporting countries were Australia, Russia and Mozambique.

Among the top buyers were the Adani Group (Adani Enterprises and Adani Power) followed by JSW Steel and Tata Steel.

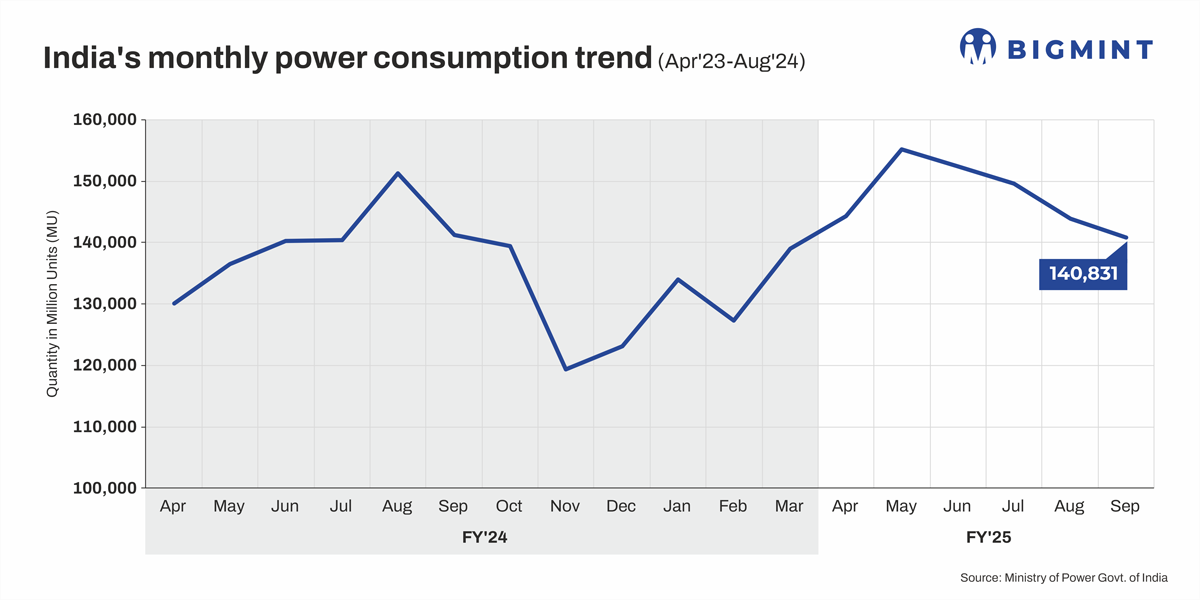

*Higher power consumption: Data collated by BigMint reveals that the country's power consumption in H1FY'25 increased by over 5% y-o-y to 886,128 million units (MU) from 839,904 MU in the

corresponding period last fiscal. In India, around 75% of power is generated by coal and higher consumption means higher coal usage and reliance on imports.

*Higher coal-based generation: According to data from the Ministry of Power, coal-based electricity

generation in the country increased by more than 8% in the first eight months of 2024 (January-August). In contrast, the total generation by large hydropower projects in the country actually decreased by over 5% during the same period. The share of renewable energy and storage systems witnessed marginal growth y-o-y. So, the higher reliance on coal was to an extent reinforced despite the rise in dispatches by state-owned Coal India (CIL) in H1 to 366.6 mnt as against 360.6 mnt in H1FY'24.

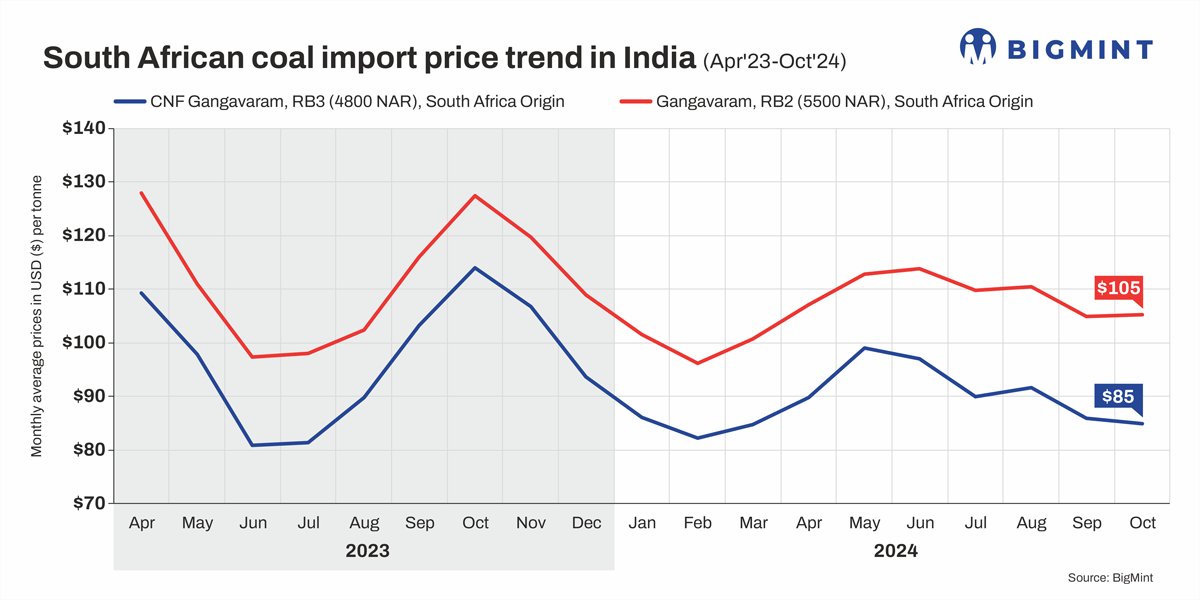

*Increased demand from steel sector: Increase in domestic sponge iron production created higher demand for imported (mainly South African) coal due to its efficiency and productivity compared to high- ash domestic coal. As per BigMint data, sponge iron output stood at 22 mnt in April-August 2024 compared with 20.6 mnt in the year-ago period. Increase in sponge iron production propelled the demand for imported coal.

Prices stayed stable which created a favourable condition for imports. Data shows that the import prices for RB2 coal remained largely stable at $109.8/t in H1FY'25 as against 108.6/t in H1 of the last fiscal.

Similarly, prices for RB3 were recorded at $92.3/t CNF Gangavaram in H1 as against $93.6/t in H1FY'24.

*Rising production in Indonesia driving exports: Despite heavy rains in Sumatra and South Kalimantan in the first quarter of 2024, Indonesian coal production in the first four months of 2024 increased by

8.6%. In 2023, Indonesia achieved record coal production of 775.18 mnt, up12.8% y-o-y. Exports stood at over 500 mnt. The government has set an ambitious production target of 922.14 mnt for 2024. Despite

rising domestic power demand in Indonesia, surplus production is getting channelled into key Asian markets which huge coal appetite, mainly China and India.

Non-coking coal imports increased by more than 5% m-o-m in September. With the monsoon finally receding in most parts of the country domestic supplies will be augmented which will act as a counterweight to imports.

However, the demand surge during the festive season will drive higher coal-based generation and imports. The turnaround in the industrial sectors coinciding with the festive season will drive the demand for restocking in order for producers to be prepared for an improved production cycle towards the end of Q3FY'25.

Source:BigMint