Posted on 15 Oct 2024

|

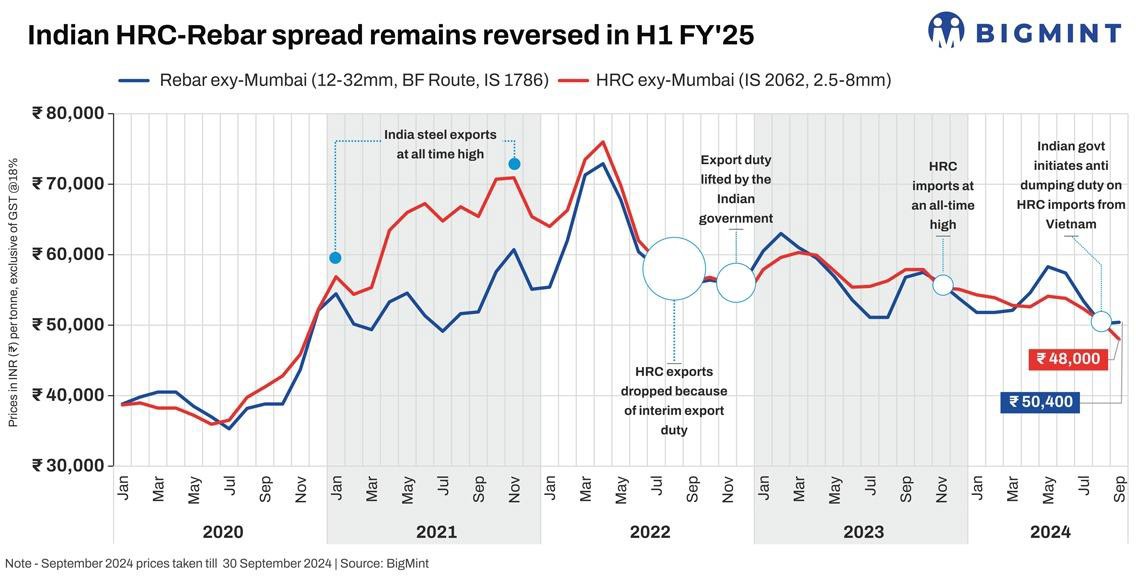

Morning Brief: The HRC-rebar spread reversed sharply again in September, 2024, after normalising in the preceding month, reveals BigMint data. Usually, hot rolled coils (HRCs) are sold at a premium to rebars.

However, HRCs consistently remained priced lower m-o-m against rebar over April- July, then increased by a mere INR 300/t ($4/t) in August, only to decrease by a sharper INR 2,400/t ($29/t) in September. On an H1FY'25 basis, rebars were stronger at INR 54,000/t ($644/t) against HRC's INR 51,880/t ($618/t).

In September, the average benchmark trade-level HRC (IS2062, 2.5-8mm) price plunged to its lowest in four years to INR 48,000/t ($572/t) since near-about levels of INR 46,000/t ($548/t) were last seen in November 2020.

The blast furnace-route rebar (12-32mm), on the other hand, fared slightly better at INR 50,400/tonne ($600/t) last month.

What factors impacted the spread in H1FY'25?

High imports, domestic supplies create demand barriers: Mills were consistently on the back-foot in H1FY'25 amid surging imports and domestic supplies and slack export movements. Tier-1 mills undertook production cuts earlier in the fiscal which allowed them to rationalise production and raise prices in May and to an extent in June.

BigMint data reveals, imports in H1FY'25 were at a significant 5.1 million tonnes with September's volumes at an estimated 1.1 mnt. In comparison, H1FY'24's figure was at a far lower 3.3 mnt. The imports influx has been creating demand obstacles for domestic mills. That apart, India also experienced a production glut in HRCs with NMDC's Nagarnar Integrated Steel Plant having started commercial production last year and commissioning of JSPL's 5.5-mtpa HSM at Angul. This double whammy in the face of sluggish demand kept HRC prices suppressed through the first half. BigMint data shows India's production of HR coils/strips and equivalents rose to a provisional 26.10 mnt in H1FY'25 against 25.70 mnt in the same period last fiscal.

Poor export performance, sliding global prices hit domestic mills: Another twin whammy exerted further pressure on domestic mills. These included a very poor export performance and sliding global prices - both factors influence domestic pricing. Exports were lower by 0.3 mnt in H1FY'25 at 0.5 mnt against 0.8 mnt in the same period last fiscal. Aggressive Chinese pricing, and lacklustre global demand amid geopolitics, volatile energy prices and environmental factors, impacted demand for Indian steel overseas. Indian mills withdrew offers to the Middle East and Vietnam, two of its key markets, again, from May this year.

Meanwhile, Chinese HRC FOB offers fell 12% y-o-y to $507/t in H1FY'25. Japanese FOB offers for HRCs dropped 10% to $541/t in this period. Vietnam's Hoa Phat's HRC offers fell from a high of $580/t CNF HCMC to $515/t in September and Formosa's, from $605/t to $517/t in this period.

Maintenance schedules take care of inventory: In rebars, prices remained somewhat more supported because of a few factors. One, mills experienced some pre-election restocking in April-June. Two, both BF and IF mills undertook production cuts to reduce inventory idling time from 12-15 days earlier in the fiscal to 6-8 in the later months. It may be noted, BF mills have been undertaking production cuts since January in a bid to restore the supply-demand imbalance that led to an inventory glut. Plus, tier-1 and larger mills have taken maintenance shutdowns from April-September, though not all together.

Liquidity, monsoon dampen demand: However, on the flipside, IF segment demand had seen a steady erosion amid post-poll liquidity issues which had also pulled down BF-grade material in some months. IF mills undertook production cuts of 20-25%.

Secondly, the monsoon period of June-September kept demand constrained. It was only from late September that mills have sensed a demand rebound.

Raw materials fail to support finished prices: Prices of all key raw materials fell y-o-y in H1FY'25. For the tier-1 mills - producers of flats, both iron ore and coking coal decreased by a higher percentage compared to IF mills' input materials. The Odisha iron ore fines index fell 7% y-o-y to INR 4,707/t ($56/t), while coking coal slid 9% to

$245/t CFR India. Sponge iron dropped 7% to INR 26,800/t ($319/t) and billets by 6% to INR 41,000/t ($489/t).

Prices may have bottomed out and can either remain stable or rise from here since the peak demand season is seen setting in from October. Construction activity is likely to resume and festivities may fuel demand for automotive and consumer durables. Some major mills have already effected hikes in flats and longs. But, it is to be seen if these will be absorbed by the market.

Source:BigMint