Posted on 24 Sep 2024

When it comes to Europe's nascent "green" steel sector, conversation for the most part has centered on flat products.

After all, flats -- including hot-rolled coils and sheets -- account for the bulk of both the continent's steel production and consumption, and the flats sector was the first to see premiums for material certified with a lower carbon profile than standard steel.

The annual combined European flat product deliveries and imports averaged around 82.96 million metric tons from 2013-2022, according to European steel producers association Eurofer. During the same period, the annual combined European long product deliveries and imports averaged about 49.58 MMt.

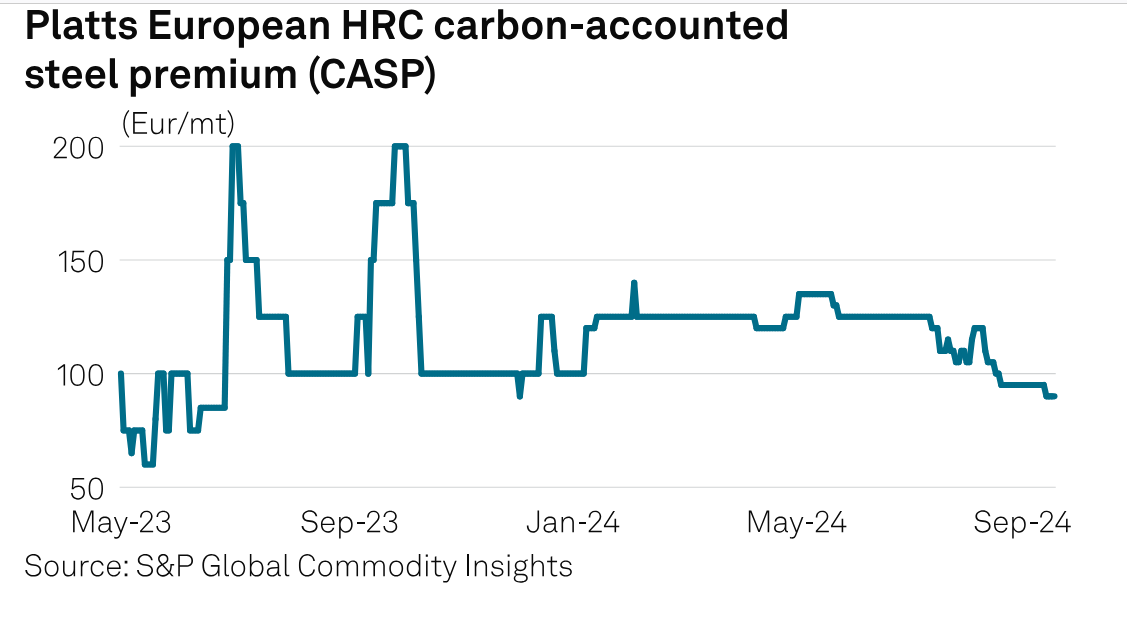

Premiums emerged last year in Europe for carbon-accounted flat steel, and Platts, part of S&P Global Commodity Insights, addressed market demand for price assessments and data to help bring transparency to trade in such products -- launching first-of-their-kind daily carbon-accounted HRC assessments in May 2023.

And now that the green conversation in Europe has extended to other markets, including long steel products used in construction, Platts has also expanded its carbon-accounted assessment offerings.

Effective Sept. 11, Platts launched new weekly spot price assessments for European carbon-accounted rebar and medium sections.

The new assessments -- which Platts understands to be the first carbon-accounted assessments for long steel -- include a European Rebar Carbon-Accounted Steel Premium (Rebar CASP), a European Medium Sections Carbon-Accounted Steel Premium (Medium Sections CASP), a Northwest Europe Rebar Carbon-Accounted Steel Price and a European Medium Sections Carbon-Accounted Steel Price.

Based on industry feedback, the European rebar and medium sections carbon-accounted steel premiums reflect any differential achieved for the spot sale of rebar and medium sections, with total accounted carbon emissions of 0.6 metric tons of CO2-equivalent, or less, for every metric ton of steel produced.

The assessments include emissions from direct, indirect and associated upstream and downstream activities, such as processing of steelmaking raw materials, hot metal production, steel rolling and associated transportation and logistics -- typically referred to by market participants as scopes 1, 2 and 3.

Carbon emissions must be certified by an internationally accepted independent organization, and market participants will be expected to supply proof of such certification upon request.

Trade in steel products using offsets to reduce overall emissions profiles, such as carbon credits sourced from voluntary carbon markets, will not be considered for inclusion in the assessments. Platts will consider trade where a mass balancing approach has been applied and validated by a certified internationally accepted independent organization.

Platts assessed the Rebar CASP at Eur40/mt, Sept. 18, down from Eur70/mt Sept. 11 and the Medium Sections CASP at Eur65/mt, Sept. 18,down from Eur92.5/mt Sept. 11.

It is easy to see why the construction sector has entered the green conversation. Construction -- which relies heavily on longs like rebar and medium sections for support -- is not only the largest end-use sector for steel, but is also one with high associated carbon emissions.

Steel production generates 7%-9% of global CO2 emissions and about 5% of overall emissions in Europe, according to the Institutional Investors Group on Climate Change.

And regulatory requirements, such as the European Union's Carbon Border Adjustment Mechanism scheme, as well as accelerated decarbonization efforts around the world, have underscored the need for heavy industries like steelmaking to move quickly to reduce carbon emissions.

In a Sept. 5 paper titled Investor Priorities for Transitioning the European Steel Sector, the IIGCC said "the steel sector's decarbonization is essential" and that "creating a supportive policy environment for the transition of high-emitting sectors is critical for achieving Europe's commitment to climate neutrality by 2050."

To stimulate low-carbon steel demand, the IIGCC said public steel procurement could be used as a tool to drive decarbonization innovation and incentivize use of low-carbon steel products. Financial incentives could include point-of-sale subsidies, tax exemptions, post-purchase rebates or tax credits, the IIGCC said.

Such investment would mirror investment made by European steelmakers offering carbon-accounted steel -- mainly through conversion to electric-arc furnaces or implementing hydrogen and fossil-free fuel production. The steelmakers that have technology upgrades and innovative steelmaking investments will be essential not only for Europe's own industry, which faces a "historic, strategic turning point," but in the global steel industry's decarbonization journey as well, IIGCC said.

"Investors see Europe as well positioned to lead the global transformation of the steel sector," it said. "The EU is a large, highly developed economy with generally high-end steel production that can seize the opportunities and show what is possible, paving the way for other regions to follow."

While the release of investment funds by the European Union and individual governments in the region have helped to kick off technical enhancements to reduce producer emissions, there are still several factors that are holding back trading activity of lower carbon emission products.

A hampering factor for the acceleration of carbon-accounted steel is the lack of an internationally adopted industry standard. Associations and trade groups such as the German steel federation and Responsible Steel have started to publish guidelines in the hope that they would become standards, but they've yet to gain widespread adoption.

A difficult economic environment seen in 2024 has meant that those who do not necessarily need to buy material with a lower carbon profile have opted for less expensive conventional steel -- or have limited their spot market buying activity.

Rising interest rates and a near-recession in Germany hit medium-sized businesses -- the so-called Mittelstand in Germany and the backbone of Europe's biggest economy. German manufacturing remains weak, while the automotive industry also is struggling.

Demand and price development for carbon-accounted steel remains deeply correlated with the conventional steel market, and in times of weak steel demand for the market at large, carbon-accounted steel remains heavily affected.

Analysts at Commodity Insights do expect some near-term upside, with a steel price recovery from December 2025 due to restocking and restricted import supply.

Once restocking activities resume and economic tightness ease, trading activity is likely to resume to previous levels, market participants contend.

It then will be up to steelmakers in Europe and abroad to execute on the vision of Europe as a global leader in the energy transition.

Source:S&P Global Commodity Insights