Posted on 23 May 2024

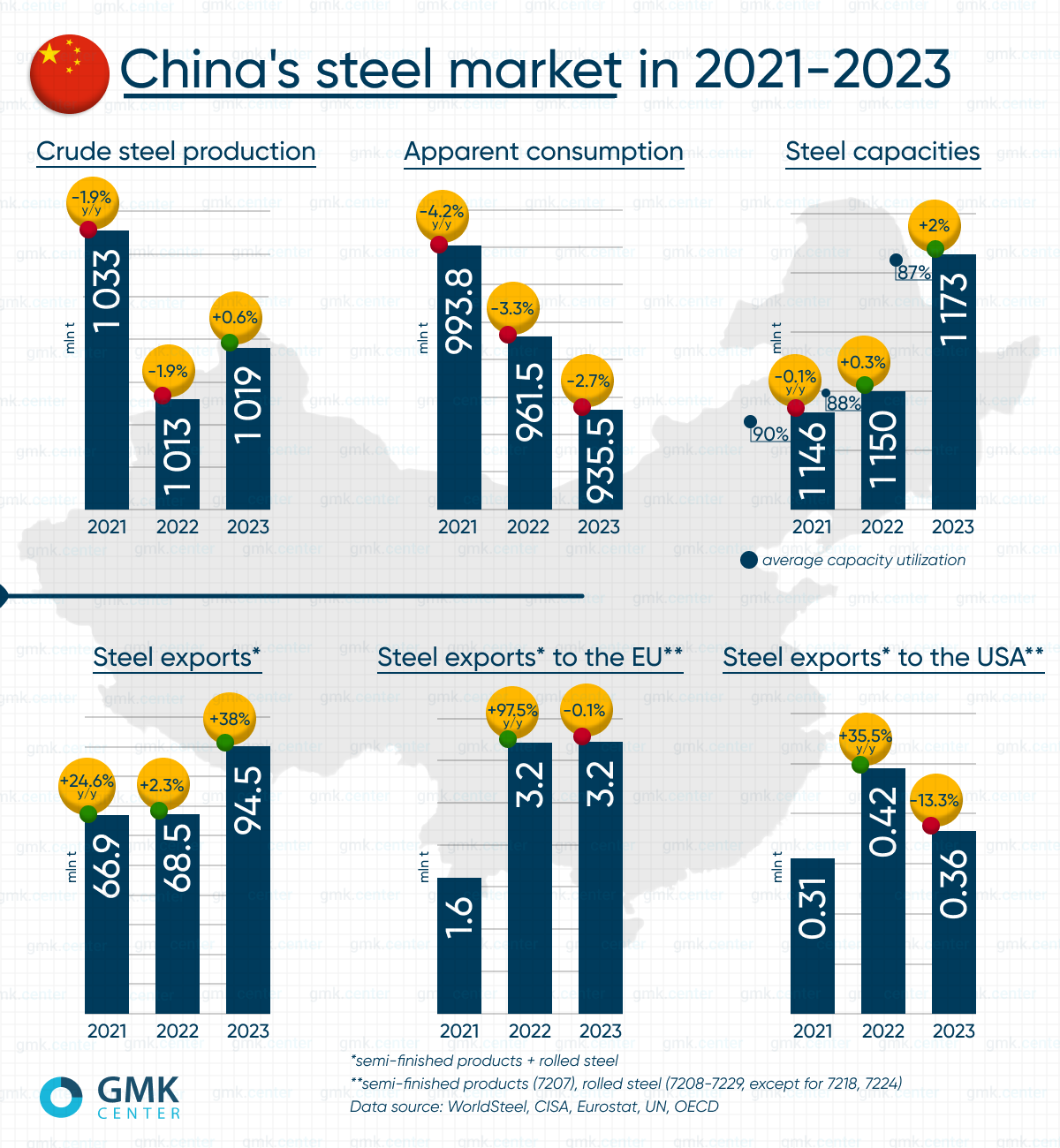

China is the world’s largest steel producer, which, according to the Global Energy Monitor, has about 500 steel mills of various types with a total capacity of about 1.17 billion tons of steel per year in 2023.

Every year, Chinese steelmakers gradually increase their production capacity, in particular, in 2021 it amounted to 1.146 billion tons, in 2022 – 1.149 million tons, and in 2023 – 1.173 billion tons. At the same time, capacity utilization is declining, creating a surplus. Thus, in 2021, this figure was 90.1%, in 2022 – 88.1%, and in 2023 – 86.9%.

China’s steel production has been gradually increasing over the past 10 years, but in 2020 it peaked at 1.065 billion tons and began a downward trend, which ended in stabilization in 2023 at 1.019 billion tons compared to 1.013 billion tons in 2022. The 2020 peak was driven by pent-up demand and the global economic recovery from the COVID-19 pandemic. Since then, the Chinese authorities have imposed restrictions on steel production to meet climate goals.

Apparent steel consumption in the country has also been declining over the past two years. Thus, in 2021, the volume of steel consumed reached 993.8 million tons, in 2022 – 961.5 million tons, and in 2023 – 935.5 million tons. That is, over 3 years, the decline amounted to 5.9% or 58.3 million tons. The main reason for this is the crisis in the country’s real estate market.

Since the rate of decline in steel consumption is much lower than in production, large volumes of unused products are exported. Thus, from 2020 to 2023, China’s steel exports almost doubled, reaching their highest level since 2016:

High exports in 2023 were driven by low prices for steel products compared to other exporting countries, as well as weak domestic demand due to problems in the construction sector observed throughout the year.

The main volumes of steel were exported to regions where there are no trade barriers, including Southeast Asia, the Middle East, South Asia, Central America, etc. They account for more than 80% of China’s steel exports.

At the same time, steel exports to the European Union have undergone dramatic changes over the past three years. In 2021, it amounted to 1.61 million tons, and in 2022 and 2023, it was 3.184 million tons and 3.181 million tons, respectively.

The EU protects its steel market through import quotas and anti-dumping measures. However, steel supplies from China to the EU grew by 97.5% y/y in 2022 and decreased by 0.1% y/y in 2023, despite many trade restrictions. This growth was caused by the difficult situation in the EU steel industry after Russia’s full-scale invasion of Ukraine. The bloc’s industry faced a sharp rise in energy prices, which, in turn, made it impossible for local products to compete with cheaper Asian ones.

Chinese steel exports to the United States have not changed dramatically over the past 3 years, although the circumstances of 2022 also gave rise to an increase in shipments:

The US is doing a much better job of protecting its domestic market from Chinese products. In particular, President Joe Biden recently instructed the U.S. Trade Representative to increase tariffs under Section 301 of the Trade Act of 1974 on $18 billion worth of imports from China. This step includes raising the tariff rate on certain steel and aluminum products of Chinese origin from 0.0-7.5% to 25% in 2024.

The issue of China’s steel export growth is much broader, as it affects global trade flows, price levels and capacity utilization around the world.

«The crisis in China has once again resulted in a new wave of trade restrictions, and not only against Chinese products. As the Asian market becomes crowded, prices are falling, and products from Korea and ASEAN countries are putting pressure on other markets. For example, Turkey or Europe. And we see how these countries react by closing their markets to everyone. For example, with protective quotas,» comments Andriy Tarasenko, Chief Analyst at GMK Center.

Source:GMK Center